Sexual Abuse and Assault Injury Lawyers

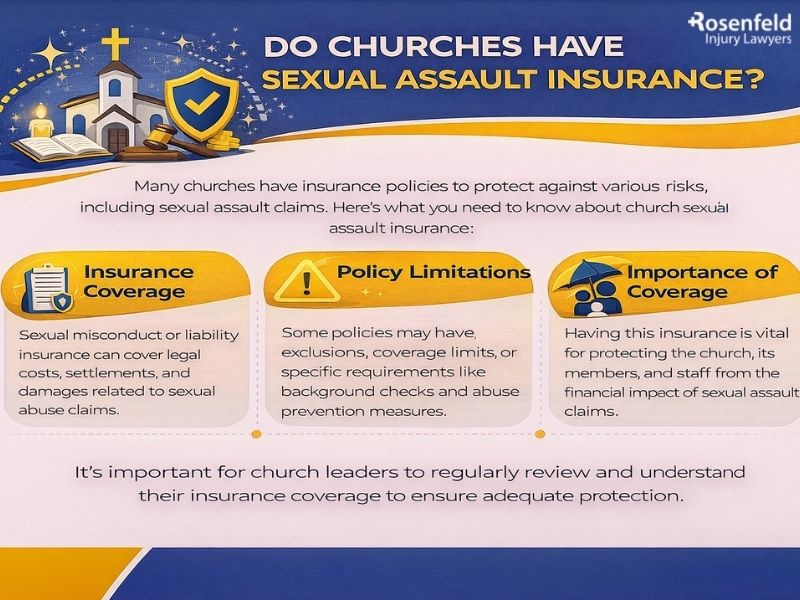

Do Churches Have Sexual Assault Insurance?

At Injury Lawyer Team, we guide survivors, families, and communities through some of the most painful and complex questions that arise after clergy abuse. One of the most common questions we hear is do churches have sexual assault insurance, and how these policies interact with the civil suit process.

We are here to help you understand what insurance coverage may apply, how churches protect their financial assets, and how we can fight for accountability.

Churches, ministries, and other non-profit organizations often maintain multiple layers of liability insurance designed to protect the organization, its leadership, and its employees from claims arising from negligence.

When those claims involve adult or child sexual abuse, special forms of sexual misconduct liability coverage become critically important. These policies affect everything from legal defense costs to settlement payments, other legal expenses, and the long-term financial protections available for victims.

Understanding Sexual Misconduct Liability Insurance Coverage for Churches

Most churches operate as non-profit organizations with structured risk-management programs. The church’s insurance policies typically include several different types of insurance coverage, each addressing different forms of risk, improper behavior, and incidents that may occur during ministry operations.

Below are the core categories of liability coverage:

General Liability Insurance

This is the most common insurance policy churches carry. It covers bodily injury, property damage, and other basic risks that occur on church premises, such as a slip-and-fall or an accident during youth activities. While general liability sometimes overlaps with sexual misconduct claims, it usually does not automatically cover sexual abuse allegations unless the policy includes specific endorsements.

Professional Liability Insurance

Some churches, especially larger ministries, rely on professional liability or pastoral counseling coverage for claims involving counseling services, emotional injury, and certain forms of improper behavior during pastoral care. This insurance can sometimes apply when clergy violate boundaries while acting in a counseling capacity.

Sexual Misconduct Liability Coverage

This is the specialized coverage most relevant to clergy sexual abuse lawsuits. It may appear under names such as:

- Sexual misconduct insurance

- Molestation insurance coverage

- Sexual abuse and molestation (SAM) endorsements

These policies are designed to respond to sexual abuse claims involving improper conduct by a youth pastor, volunteer, teacher, minister, or other church employee. This is the coverage that pays legal defense, litigation expenses, settlements, and sometimes excess coverage if the church’s primary limits are exhausted.

Specialized Denominational or Group Risk Pools

Some religious organizations participate in risk-sharing pools that provide a shared layer of monetary protection. These plans often include important coverage for sexual misconduct, provided the church meets specific risk-management conditions, such as background checks, training, and reporting procedures.

Together, these policies form the essential protection churches use to manage potential risks involving children, youth pastors, and ministries that serve vulnerable people.

How Are Child Sexual Abuse Settlements Involving Youth Pastors and Other Clergy Paid

In childhood sexual abuse cases involving clergy, settlement payments usually come from a combination of insurance layers and church assets. Here is how it typically works when a survivor files a civil suit:

Primary Sexual Misconduct Liability Insurance

Most churches have a primary policy that covers:

- Institutional negligence

- Negligent hiring, supervision, or retention

- Failures in reporting

- Harm caused by the lack of criminal background checks

- Bodily injury and emotional injury suffered by victims

This primary coverage often compensates the first layer of settlement funds.

Supplemental or Excess Endorsements

Some churches have additional endorsements offering higher limits. These endorsements allow insurance to finance larger settlements when the harm is severe or when the organization’s negligence deeply affected the survivor’s life.

Umbrella or Excess Liability Policies

Umbrella policies act as a safety net when the primary policy is exhausted. Many ministries, especially large organizations, carry umbrella insurance because sexual abuse settlements can be substantial.

Denominational Risk Pools

Certain denominations fund settlements through pooled insurance systems. This helps smaller churches access higher levels of financial resources and liability coverage.

Church Assets

Insurance does not cover intentional acts by the perpetrator. The offender’s intentional abuse is excluded from coverage, but the organization is still responsible for its own negligence. If insurance funds run out or if the church fails to purchase the right coverage, remaining amounts may be paid from church assets. Some ministries even face bankruptcy after large abuse settlements if they lack adequate protection.

How Does Retroactive Coverage Work for Clergy Child Abuse?

When the abuse happened years or decades ago, retroactive coverage becomes one of the most important factors in determining whether a church’s insurance can still pay.

Two primary forms of liability insurance determine whether the claim is covered:

Occurrence-Based Policies

These policies apply if the abuse occurred during the coverage period, even if the victim files the claim many years later. Many older church policies were written on an occurrence basis, which is essential for historic claims because childhood sexual abuse is often reported only later in adult life.

Claims-Made Policies

These policies apply only if the claim is both made and reported during the coverage year. This makes historic abuse cases much more complicated, because the coverage may no longer exist unless the church purchased tail coverage or special extensions.

Why Retroactive Coverage Matters

Retroactive coverage ensures that past misconduct is still covered under certain policies. When we handle sexual abuse allegations related to historic misconduct, we often investigate:

- Whether the church maintained continuous policies

- Whether retroactive dates limit coverage

- How insurance agents sold or modified the coverage

- Whether ministries’ end endorsements were properly applied

Identifying historical coverage can significantly increase the financial resources available to survivors.

Molestation Coverage and Abuse Endorsements Used by Religious Institutions

Most churches are required by insurers to implement strict protocols in order to maintain molestation coverage or sexual misconduct insurance. These risk-management requirements exist because churches serve children and operate youth activities that involve close contact with vulnerable individuals.

Common requirements include:

- Written child-protection procedures

- Criminal screening checks for youth pastors, volunteers, and employees

- Training on recognizing abuse

- Reporting protocols

- Supervision standards for youth programs

- Screening of all adults participating in ministry

- Separation-of-duties rules to protect children

- Safety policies for overnight events

Insurance companies know that churches face potential risks due to frequent interactions between clergy, staff, and children. That is why they require these safeguards before agreeing to cover sexual misconduct risks.

If the church violates these procedures, the insurer may attempt to deny coverage. We frequently challenge these denials.

How Does Sexual Harassment Liability Coverage Work?

Sexual harassment claims are treated differently from acts of sexual abuse. Harassment claims often involve:

- Employees

- Supervisors

- Pastoral staff

- Complaints of improper comments, touching, or boundary violations

- Hostile work environments

These claims usually fall under employment practices liability insurance (EPLI). Unlike abuse policies, EPLI focuses on workplace dynamics, including allegations involving clergy members acting as supervisors or leaders.

While sexual misconduct liability insurance covers certain forms of abuse, harassment is viewed through an employment lens. Both forms carry serious legal, emotional, and financial concerns.

How Injury Lawyer Team Can Help

When survivors come to us, they often feel overwhelmed by the complexity of liability, insurance, reporting failures, and church leadership. We stand with you, we’re here to listen, and we believe in your case.

In every matter involving specific needs of clergy sexual abuse lawsuits, our role includes:

Identifying All Applicable Policies

We examine every insurance policy the church carried: general liability, professional liability, sexual misconduct coverage, umbrella policies, risk-pool memberships, and anything else that may offer financial protection.

Pursuing Multiple Insured Entities

Many cases involve multiple organizations, including local churches, parent ministries, diocesan structures, and faith-based nonprofits. We look at every organization involved to maximize available coverage.

Challenging Denials and Insurance Defenses

Insurers sometimes deny coverage, arguing that the church failed to follow protocols or failed to purchase the right coverage. We fight these denials, gather the necessary evidence, and make the strongest case for full compensation.

Addressing Legal Defense Issues

We ensure that the church’s insurer does not misuse legal defense tactics to delay or deny justice. Our focus is always forward-thinking: protecting our clients, advancing your claims, and keeping your well-being at the center.

Protecting Survivor Privacy

Confidentiality is essential. We ensure your identity is protected wherever possible, especially in cases involving children or deeply personal trauma.

Trauma-Informed Representation

You’re not alone. We guide you through each step of the civil lawsuit process with compassion, clarity, and strength.

Contact Us

If you or a person you love has been harmed by clergy or church personnel, or if you’re navigating questions about laws, insurance, negligence, or accountability, please reach out. We’re here to support you in court with strength, compassion, and an unwavering commitment to justice.

We handle these cases on a contingency fee basis, meaning you pay no upfront legal costs and no attorney fees unless we successfully recover compensation for you. Contact Injury Lawyer Team when you’re ready for your free and confidential consultation.

All content undergoes thorough legal review by experienced attorneys, including Jonathan Rosenfeld. With 25 years of experience in personal injury law and over 100 years of combined legal expertise within our team, we ensure that every article is legally accurate, compliant, and reflects current legal standards.