Does Insurance Cover Sexual Assault Claims?

At Injury Lawyer Team, we stand with survivors seeking clarity, safety, and accountability. Many of our clients come to us asking: Does insurance cover sexual assault claims, and what role does insurance coverage play in sexual abuse lawsuits?

These questions matter because survivors often worry that the individual abuser will never have the financial resources to compensate them, and that pursuing a civil case may not lead to meaningful recovery.

This article explores how liability insurance can provide coverage for sexual harassment cases, why institutions often carry commercial general liability policies designed to protect them from negligence claims, and how our firm helps survivors determine every available path to financial relief. We believe in your case, and we guide you through every step of the legal system with care and confidentiality.

How Insurance Coverage Works in Civil Sexual Abuse Lawsuits

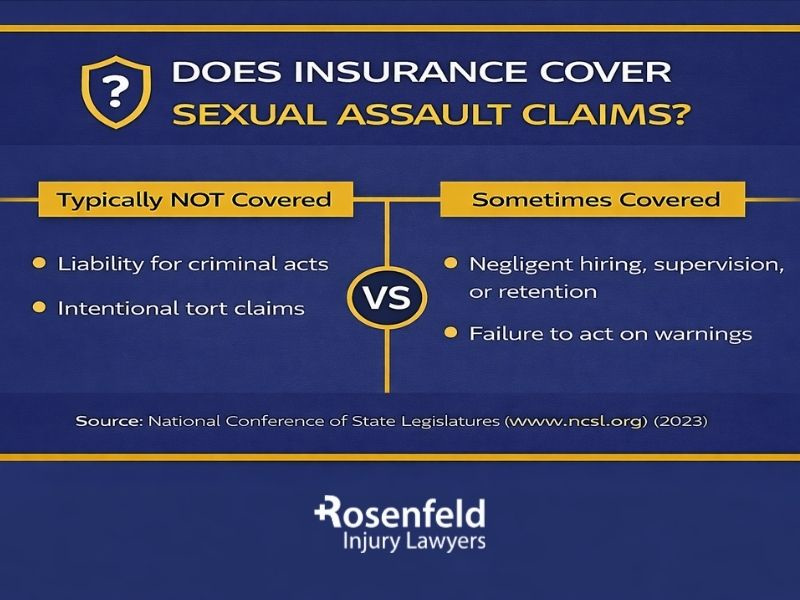

Insurance companies pay for civil sexual harassment claims when the insured person or institution purchased an insurance policy that covers their negligence. This is a critical distinction. While willful acts, such as rape, sexual molestation, or other forms of intentional conduct, cannot be insured, negligence by institutions, employers, supervisors, or property owners can be covered.

In most sexual abuse claims, the underlying claim is based on a perpetrator’s wrongful acts. However, coverage under an insurance policy is activated when a plaintiff alleges that a school, church, youth program, or business violated its duty to protect the survivor by committing negligent supervision, negligent security, or negligent hiring.

In other words:

- Intentional acts by an abuser are excluded

- Negligent acts by an institution or employer are covered

Because most sexual harassment cases involve both intentional abuse and institutional negligence, liability insurance often becomes one of the primary sources of recovery in civil litigation. The law recognizes that institutions have responsibilities to protect people from foreseeable harm. When they fail, insurance is there to provide coverage.

Which Types of Insurance May Cover Sexual Assault Cases?

Insurance coverage in sexual harassment claims varies by policy type, contractual phrasing, exclusions, and state statute. Below are the most common forms of coverage we identify while representing our clients.

Commercial General Liability Policies

These policies, commonly called CGL policies, are purchased by schools, churches, youth programs, businesses, and other organizations. A CGL policy typically insures:

- Bodily injury, including emotional distress

- Negligent hiring, oversight, and retention

- Failure to warn or failure to protect

- False imprisonment in certain abuse scenarios

- Liability for loss caused by the organization’s negligence

CGL coverage does not insure intentional criminal conduct like sexual harassment, assault, or abuse. However, business insurance under a CGL policy does cover claims when the lawsuit is based on the employer’s or organization’s negligence, not the perpetrator’s intent.

This distinction is central to how survivors secure compensation in sex abuse cases.

Sexual Misconduct Liability Endorsements

In recent years, institutions such as youth programs, religious organizations, camps, daycare centers, and treatment facilities have increasingly purchased sexual misconduct liability endorsements, special add-on policies that specifically cover:

- Abuse allegations

- Negligent oversight leading to sexual misconduct

- Damages arising from an employee’s sexual misconduct

- Failures in the organization’s reporting structure

These endorsements may expand coverage beyond what a standard CGL policy provides. They often respond even when the district court or insurer disputes whether a negligent act occurred, so long as the victim alleged institutional wrongdoing.

Malpractice / Professional Liability Insurance

Professionals such as therapists, doctors, nurses, counselors, and psychologists often carry malpractice insurance that can cover negligent acts related to boundary violations, improper treatment, or professional misconduct. Although malpractice insurance cannot insure intentional assaultive sexual conduct, courts have found that insurance may respond when:

- The survivor alleged negligent treatment

- The abuse occurred during therapy or medical care

- The policy text includes “professional services” coverage

We frequently see malpractice insurers defend such claims under reservation of rights while the court determines how to interpret exclusions.

Homeowner’s or Renter’s Insurance

These policies come with substantial limitations and rarely cover intentional abuse, but they sometimes apply when:

- A homeowner negligently supervised a minor

- A renter failed to prevent foreseeable misconduct

- A property owner ignored known risks

Actual coverage is extremely limited, and exclusions for willful or intentional acts often apply. Still, we evaluate these policies carefully because insurance can make a meaningful difference when a survivor’s injuries occurred in a private residence.

Vicarious Liability and When Business Insurance Pays for Sexual Harassment and Assault Claims

One of the most important legal theories in sexual harassment claims is vicarious liability. This occurs when an insured employer is responsible for the conduct of its employees, even when the employer did not commit the wrongful act itself.

Courts look closely at:

- The employee’s role

- The employer’s supervision

- Whether the employer was aware of misconduct

- Whether the employer failed to protect clients or visitors

When survivors sue under the following theories, insurance typically responds because these claims arise out of employment, not the perpetrator’s intent:

- Negligent hiring

- Negligent supervision

- Negligent security

- Failure to warn

- Failure to report

Even if the perpetrator’s intentional acts were criminal and led to criminal prosecution, the institution can still be held liable for its own negligence. In many cases, courts held that legal policy considerations allow victims to recover from institutions because negligence, not the sexual misconduct itself, is the covered event.

This is why survivors frequently pursue business insurance, excess insurance, and umbrella policies to secure full compensation.

Insurance Policy Language Covering the Perpetrator Directly

Although rare, some insurance policies can indirectly provide coverage involving the perpetrator when the claim is framed properly. Courts across the country have examined complicated policy language related to:

- “Acts of an insured” exclusions

- “Occurrence” definitions

- Whether emotional distress is compensable

- Distinctions between intent and negligence

Coverage may apply when:

- The abuser is a professional covered by malpractice insurance

- The homeowner’s policy has negligence carve-outs

- State law interprets exclusions narrowly

- The victim alleged negligence in addition to intentional harm

Still, most courts find that intentional conduct or sexual misconduct cannot be insured because of societal policy principles. Survivors deserve protection, and insurers cannot encourage wrongdoing by providing coverage for deliberate abuse.

Thus, while we always examine every possible policy, coverage provided directly for a perpetrator is extremely limited.

When Insurance Companies Deny Sexual Abuse Claims

Unfortunately, insurers regularly deny coverage in sexual misconduct cases. Common justifications include:

Intentional-Act Exclusions

Insurers argue that all harm arose from intentional acts and that the abuse, not the negligence, is the trigger for coverage. We frequently challenge this argument because courts often distinguish the institution’s negligence as a separate, covered cause.

Claims Outside the Policy Period

The insurer claims the incident occurred before or after coverage was active. In sexual misconduct cases, this often becomes complex when abuse occurred over long periods.

Late Reporting or Misrepresentation

Institutions sometimes delay reporting abuse to their insurer out of fear, image protection, or internal mishandling. Insurers then try to deny coverage based on lack of cooperation.

Employee Exclusions or Employer Knowledge

An insurer may allege the employer was aware of misconduct or that the abuser was an employee whose intentional acts void coverage. Courts frequently examine whether the employer’s negligence created a separate basis for coverage.

Public Policy and Criminal Conduct

Some insurers claim that public policy prohibits covering assaults. However, courts repeatedly differentiate between the abuse itself and the institution’s failure to protect survivors, allowing negligence claims to move forward.

These denials are often contestable, and litigation may be necessary to secure payment.

How Injury Lawyer Team Can Help

When survivors come to us after being sexually abused, our experienced attorneys help them navigate the emotional trauma, as well as the entire insurance landscape. We know how overwhelming insurance policies can feel, especially when organizations or insurers try to hide behind exclusions, restrictions, or complex insurance terms and conditions.

In every case, we provide:

Identifying All Applicable Policies

We examine every potential source of coverage, including CGL policies, sexual misconduct endorsements, malpractice policies, umbrella policies, and any insurance the perpetrator or institution may have held.

Pursuing Multiple Defendants

Sexual abuse lawsuits often involve several responsible parties: the abuser, the institution, supervisors, security providers, treatment centers, or employers. We pursue all avenues to strengthen the underlying claim.

Challenging Coverage Denials

We litigate when insurers improperly deny claims, applying case law, statutory interpretation, and legal precedent to demonstrate why coverage should apply.

Leveraging Institutional Liability

Institutions have legal duties to protect people from foreseeable harm. We hold them accountable when they fail to act, ignore warning signs, or enable sexual misconduct.

Exploring Excess and Umbrella Policies

Many organizations carry secondary or excess policies that provide additional compensation once primary coverage limits are reached.

Throughout the process, we stand with you. We handle sexual abuse lawsuits on a contingency fee basis, meaning you pay no upfront costs and no legal fees unless we recover compensation for you. If you’re ready to talk, we offer a free consultation and a confidential space to understand your rights, pursue accountability, and move toward healing.

All content undergoes thorough legal review by experienced attorneys, including Jonathan Rosenfeld. With 25 years of experience in personal injury law and over 100 years of combined legal expertise within our team, we ensure that every article is legally accurate, compliant, and reflects current legal standards.